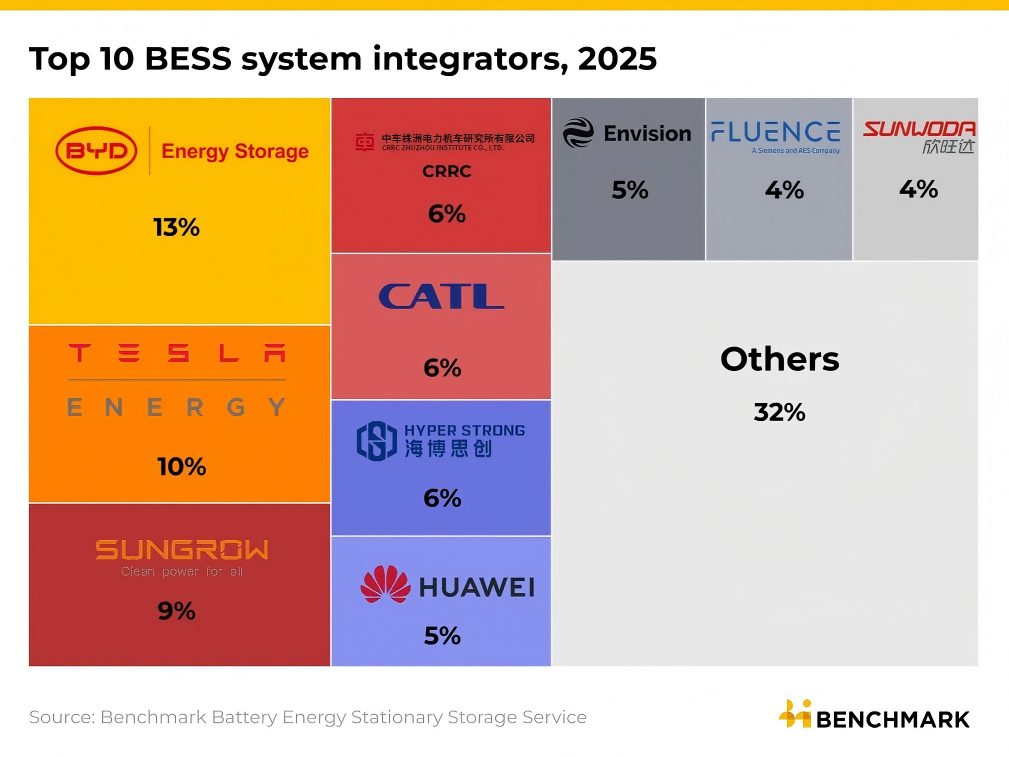

According to the latest statistics released by the authoritative research firm Benchmark Mineral Intelligence, BYD officially surpassed Tesla as the world’s leading battery energy storage system integrator in 2025, ranking first with shipments exceeding 60 GWh and a market share of 13%. This shift ended Tesla’s two-year consecutive lead from 2023 to 2024. During the same period, Tesla’s energy storage installed capacity stood at 46.7 GWh, with a market share of 10%, ranking second globally.

This shift in rankings occurred against the backdrop of rapid expansion in the global energy storage market. In 2025, global battery energy storage system installations surged by 51% year-over-year to approximately 315 GWh, while shipments of stationary energy storage cells exceeded 600 GWh. Amid this explosive growth, the Chinese market emerged as the core driving force. In December 2025 alone, the installed capacity of large-scale energy storage projects in China reached 65 GWh—a figure that even surpassed the total annual energy storage installations in the United States.

The key to BYD’s ability to overtake its competitors lies in the advantages of its vertically integrated industrial chain. Data shows that in the first three quarters of 2025, BYD’s total battery production exceeded 113 GWh, with this capacity simultaneously supporting the rapid expansion of both its electric vehicle and energy storage businesses. The model of independently researching, developing, and manufacturing Blade lithium iron phosphate battery cells not only gives BYD a structural advantage in cost control but also provides the company with greater confidence when launching high-capacity products. For example, the “Haohan” energy storage system launched in September 2025 features a standard capacity of 14.5 MWh—approximately three times that of Tesla’s Megapack product released during the same period—and has already been successfully deployed in massive overseas projects such as a 12.5 GWh facility in Saudi Arabia.

In contrast, although Tesla maintained a robust year-over-year growth rate of 49% in 2025 and plans to increase its annual energy storage production capacity to 50 GWh by the end of 2026, its supply chain weaknesses remain evident. Due to a long-standing lack of in-house battery cell production capabilities, Tesla’s Megapack products rely primarily on external procurement, with its cell suppliers even including BYD and CATL—its direct competitors in the energy storage sector. To alleviate this situation, Tesla recently finalized a multi-billion-dollar lithium iron phosphate battery procurement agreement with LG Energy Solution; however, this reflects that the company remains dependent on upstream supply chains for core components.

Looking at the overall list of the top ten companies in the global energy storage industry, Chinese firms now occupy eight spots. In addition to BYD, companies such as Sungrow, CRRC Zhuzhou Institute, CATL, and Huawei are all on the list.